Thank you Lexington Law Firm for sponsoring this post.

A high service partner and consumer advocate that will help you fight for the credit you deserve!

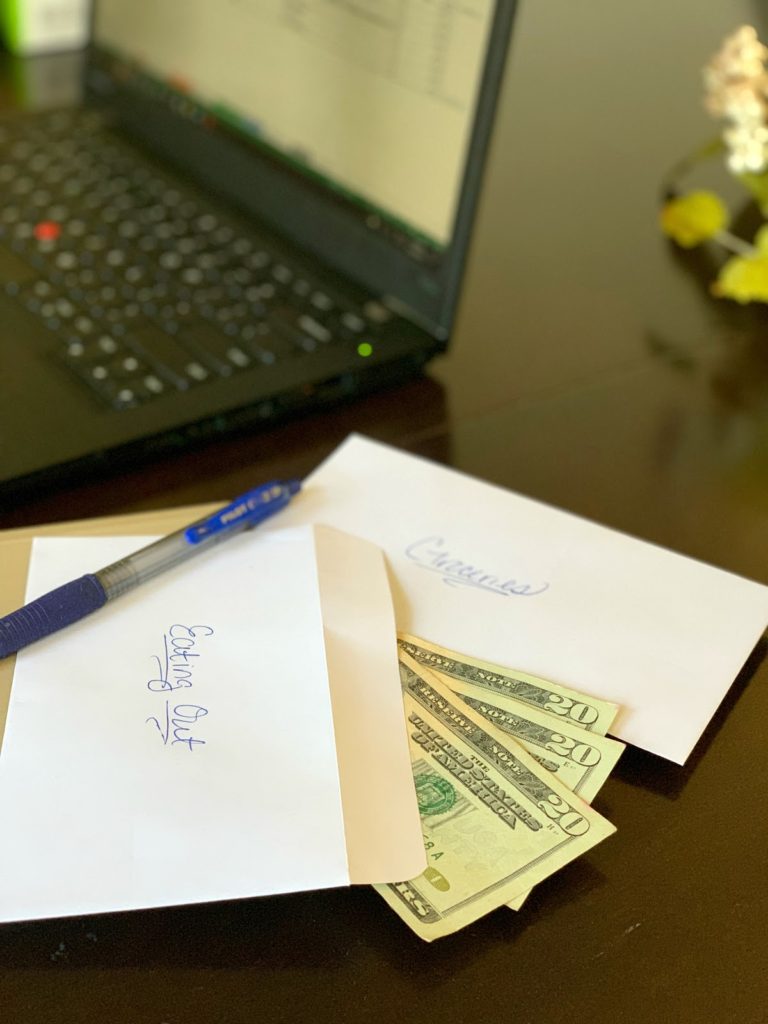

Last year, my husband and I talked a lot about what would be required for us to feel like we were financially free and we made a huge commitment to do what was necessary to reach our financial goals over the course of the next few years. We budget and have financial meetings to discuss where things stand, we use the envelope system for items that could easily get out of hand, and we have an emergency fund for unexpected things that may come our way. We talk this constantly, all to ensure that we are able to provide our two beautiful girls with a better life than what we had. They certainly keep us motivated.

So, as we continue on our journey to becoming financially free we are now specifically and personally focused on taking care of the following:

- Repairing our credit,

- Paying down our mortgage quickly (15 yrs vs. 30 yrs), and

- Paying off student loans and medical bills.

The plan was for us to spend 2018 working on the 1st item, and to shift our focus to the 2nd item in 2019. But we’ve had some bumps along the way, so we’ve reviewed, adjusted and will continue to work on repairing our credit during the first half of this year. To repair our credit my main focus has been on understanding what items and habits were causing our credit score to not be where we’d like for it to be. We then determined that we needed to manage the five areas below better if we wanted to increase our credit scores:

Credit Card Usage (i.e., Credit Utilization)

The amount of credit you use compared to the amount of your credit limit defines your credit card usage. If you divide the balance on a card by the card’s limit and multiply by 100 you’ll find the percentage of your credit utilization.

In our case, we were maxed out on a few of our credit cards so our utilization was in the area of 80% to 90% for some cards. In order to repair our credit, it was critical for us to reduce all cards, one by one, to below 30% utilization as soon as possible, with our ultimate goal being to reduce our utilization to less than 10%. So for instance, if a card’s limit was $1000 we would have a balance of $800 – $900 and would have to work to get the balance below $300 then eventually below $100. But think larger limits in our case, so we’ve really had to be disciplined and strategic about how to get each card down, and not use them again when emergencies strike.

Payment History

When it comes to payment history, it’s all about paying your bills on time, which really starts with budgeting. Although we’ve been pretty good about budgeting and managing on-time payment for years, we still reviewed each credit card we had to ensure that they were all set to be auto-drafted and that more than the minimum balance would be paid. It may not seem like a big deal to have a late payment or derogatory mark from a creditor on your report here and there, but it does have an impact and can have long-standing effects since some items can remain on your report for seven years.

So paying on time is key. It’s also critical that you ensure any items that have gone into collections are being taken care of. In this case, I suggest working with a firm like Lexington Law Firm so that you can get a full view of what is included in your report and to get help developing a strategy to ensure all items (e.g., loans, collections, inquiries, errors, etc.) are being addressed (e.g., paid, corrected, removed, etc.). Lexington Law Firm makes it easy since they have a propriety app, designed with the consumer’s needs in mind, to give you real-time solutions to help repair your credit.

Credit Errors

Sometimes, there are items on your credit report that don’t belong. It could be something small that you think doesn’t matter but everything on your report has an impact. So this is an area where I believe it’s best to seek out a partner like Lexington Law Firm to help advocate for you and work to get errors corrected and removed from your report. Errors as simple as having an address listed that doesn’t belong to you, and accounts/collections that you did not open should be addressed as soon as possible.

Trying to work with each credit bureau to fix errors can be difficult and time-consuming when done on your own. Lexington Law Firm provides free personalized credit consultation, free credit report review and recommended solutions. They believe that you have a right to a fair and substantiated credit report and have the knowledge needed to help you fight for your rights to good credit. This is the one area where I refuse to work on my credit repair alone as there is only so much I can gather from books and the internet about credit repair and the various laws associated with ensuring my report is accurate.

Hard Inquiries

We create a hard inquiry on our credit reports when lenders must review our credit to obtain loans, credit cards, cars, mortgages, and various other items that require financing. Hard inquiries have the potential to reduce your credit score, so we’ve opted to not apply for any credit for the next couple of years up until we’re ready to purchase our next home.

We specifically have to ensure that we aren’t tempted by department store credit cards (my personal issue) or the need to purchase new vehicles (since our cars are fairly old). These are our weak areas. It’s important to know where your weak areas are so that you can put measures in place to avoid pitfalls.

Credit Age

One’s credit age is the average amount of time your accounts have been open. Creditors want to see that you have been able to manage credit and do so well over a long period of time. This is one of those areas that is hard to control since your history starts whenever you first started obtaining credit. However, you can ensure that your average age stays high by not constantly opening new accounts (which create a hard inquiry that you wouldn’t want anyway). My husband and I have a credit age of about 14 years, so it’s the one area we haven’t had to worry too much about outside of making sure we don’t lower the average with new accounts.

We’ve worked diligently throughout 2018 to repair our credit and we’ve made some great strides, and have slowly been increasing our score, 10, 20 and sometimes 40 points at a times. It has been exciting to see the rewards of our efforts over time. And, it’s key to remember that it does take time. I think it’s also important to note that we spent time reading and researching, followed by months of trying to repair our credit on our own.

I believe being financially free can open up so many doors for us to do the things we really want to do including spending more time with our family and friends, traveling and doing things we’re passionate about versus constantly feeling like we’re just working to pay bills and debt. We still have a full year ahead to work towards our financial goals, and get a step closer to making financial freedom a reality. I’m confident that with the right support, we can do this, and so can you!

{kind=link}

Having bad credit is one of my biggest worries, especially as I work to carry over my student loan from university. Thanks for sharing these tips!

these are great tips and pointers for dealing with bad credit!

Credit cards are all over the place; figures demonstrate that the normal card client has more than 4 credit cards in their wallet, and there are more cards dependably available for use!prepaid gift balance register card